In 1999, a banker at JPMorgan Chase received a piece of metal in the mail.

Not a letter, not a contract, a card made of titanium, weighing 27 g. Credit Cards It had

Chapter 2: Level 1: Entry-Level Credit Cards

no credit limit printed on it because the credit limit was whatever you need.

The card was the palladium and it was sent to fewer than 10,000 people in the world. That is the top of the credit card hierarchy. Today, I’m breaking down the seven levels of credit cards. From the card, anyone can get to the cards that require an invitation. Let’s get into it.

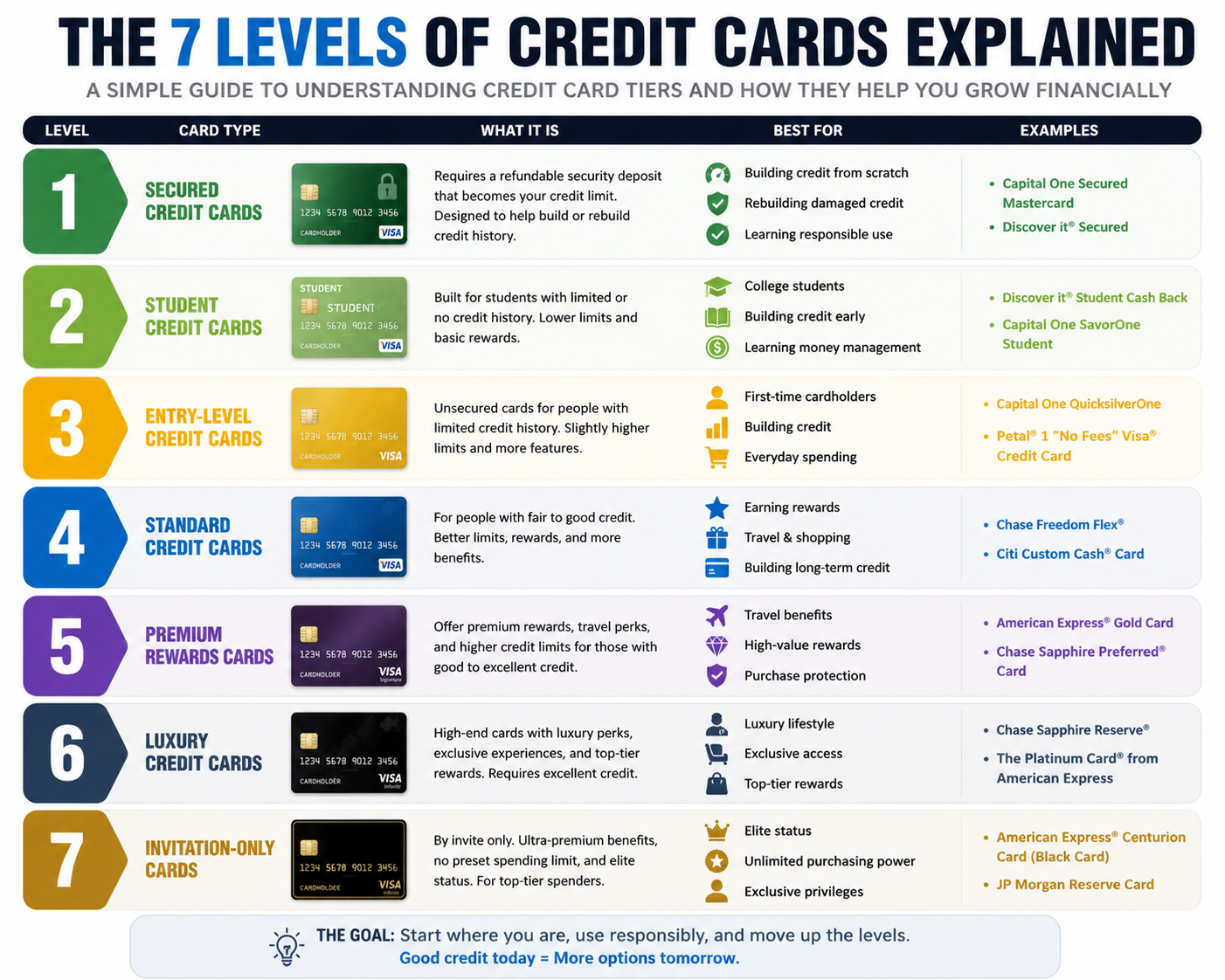

Level one, the entry-level card.

This is where most people begin their relationship with credit and where most people form opinions about credit cards that they carry for the rest of their financial lives, usually incorrectly.

A secured card requires a deposit. You put down $200, you get a $200 credit limit, and the bank takes approximately zero risk because they’re lending you your own money back with extra steps.

Capital One secured Mastercard, Discover Financial Services it Secured, the Open Sky. These cards exist for one purpose. To build a credit history for someone who doesn’t have one or to rebuild one for someone who damaged theirs. There are no rewards.

There are no benefits. There is no lounge access. Here’s what most people miss about level one.

Chapter 3: Level 2: Everyday Rewards Cards

The card is not the product. The credit score is the product. That score is the real asset being built. Who carries this? The 22-year-old who just graduated and discovered that having no credit history is treated roughly the same as having bad credit. The person who had something go wrong. A medical bill, a job loss, a difficult period. None of them are here by choice. All of them are here for a reason.

Level two, the Chase Freedom.

The Citi Double Cash. The Discover it Cash Back. Cards that cost nothing to hold, give something back for every dollar spent and represent the single most rational financial product at this tier for the majority of American households. The Citi Double Cash gives 2% back on everything, 2 cents on every dollar automatically with no annual fee.

The card is a passive income machine for people who pay their balance in full every month. The Chase Freedom Flex operates on rotating 5% categories. Groceries one quarter, gas the next, Amazon after that. It requires attention. Who carries these? Everyone

Chapter 4: Level 3: Travel Rewards Cards

who read one personal finance article in 2019 and decided they were going to optimize their spending. Some of them actually did. Most of them carry the card, forget about the categories, collect $180 in cash back at the end of the year, and feel like they won something. They did win something, just not as much as the article promised.

Level three, the Chase Sapphire Preferred, the Capital One Venture, the American Express Gold, annual fees of $95 to $250.

Points that transfer to airlines and hotels. The American Express Gold at $250 per year earns four times points at restaurants and grocery stores. For a household that spends $1,500 per month in those categories, that’s 72,000 membership rewards points per year.

Transferred to All Nippon Airways and redeemed for business class to Japan, those points are worth approximately $2,400 in travel value. The card cost $250.

The net benefit for a traveler who optimizes is substantial. The problem is that a traveler who optimizes describes about 15% of card holders. Here’s the insight that most people in this category miss.

Chapter 5: Why Transfer Partners Matter

The card is not the product. The transfer partner is the product. The card is a mechanism for accumulating currency. Where you spend that currency determines whether the card was worth carrying. If you’re finding this useful, hit the like button and subscribe. Now, back to it because this is where the cards start getting interesting.

Level four, Chase Sapphire Reserve, the American Express Platinum, annual fees of $550 to $695, airport lounge access, travel credits, global entry reimbursement, the level where the card starts providing an experience, not just points.

The Amex Platinum at $695 per year comes with $200 in airline fee credits, $200 in Uber credits, and access to Centurion Lounges. The math on the credits, if you use all of them, offsets most of the annual fee. The Chase Sapphire Reserve at $550 per year gives a $300 annual travel credit that is so broadly defined it triggers on gas stations, parking, and transit in addition to flights that most card holders hit it by April without trying.

Chapter 7: Level 5: Ultra-Premium Business Cards

Trip delay and cancellation insurance that is not theoretical. Who actually extracts value here? The consultant who flies every week and has learned that 45 minutes in a Centurion lounge before a flight is the difference between arriving at the meeting functional and arriving at the meeting having eaten a $22 airport sandwich in a gate area next to a toddler having a philosophical crisis.

The annual fee is a rounding error on her travel budget and a significant contribution to her mental health.

Level five, the American Express Business Platinum, the Citi Prestige in its final form, the Chase Sapphire Reserve for Business. Annual fees of $695 to $895.

The Amex Business Platinum at $695 per year adds 1.5 times points on purchases over $5,000. The card also comes with access to the global lounge collection, Dell credits, Adobe credits, annual airline credits.

Chapter 8: When Credit Cards Become Business Infrastructure

At level five, the card holder optimizes their business spending and personal spending simultaneously through a single instrument. The CFO approves the annual fee as a business expense. The points fund the card holders personal travel.

Chapter 9: Level 6: The Black Card Tier

Level six, the invitation-only tier, the American Express Centurion, the black card, $10,000 initiation fee, $5,000 annual fee. Amex decides when you qualify and when you do. A package arrives in the mail containing a card made of anodized titanium and a letter explaining what you now have access to.

A dedicated Centurion agent who handles travel bookings, restaurant reservations, and the kinds of requests that fall outside what a normal concierge can accommodate. Complimentary companion tickets on select airlines. Access to events that are not publicly available, fashion weeks, sporting events, cultural occasions where the access itself is the benefit and the seat is secondary.

Here is what the card actually is at this level. A signal. The person who hands a black card to a restaurant, a hotel, or a business associate is communicating something that has nothing to do with the rewards rate. The question it answers has nothing to do with points.

Chapter 10: Level 7: Private Banking Cards

The question it answers is, who is this person?

Level seven. The private banking cards, JPMorgan Chase Reserve, the Coutts World Silk Card in the UK, cards issued exclusively to private banking clients with minimum assets under management of $10 million. These are not applications. They are conversations.

Your private banker mentions at some point in the relationship that there is a card available. You express interest. It appears.

The JPMorgan Reserve issued to private banking clients of JPMorgan Chase. No published credit limit, no application. They are using a payment instrument that comes with a relationship to one of the largest financial institutions in the world. And that relationship is the product.

Here is the final insight. At level one, the card is a tool for building credit. At level seven, the card is proof that you don’t need credit. The card was never

Chapter 11: The Real Purpose of Credit Cards

the point. The relationship behind the card is.

The credit card was invented in 1950. Diners Club International, a cardboard card you could use at 27 restaurants in New York City. The founding story is that Frank McNamara forgot his wallet at dinner and found the experience humiliating enough to create an entirely new financial category.

A 22-year-old with a secured card and a $500 limit and a person who receives a titanium card in the mail from JPMorgan Chase are both participating in the same system. One is building access to it. The other has built enough of it that the system comes to them.

Chapter 12: Final Thoughts & Outro

If this was useful, subscribe. See you in the next one.